Dashboard

Weak Long Term Fundamental Strength with an average Return on Capital Employed (ROCE) of 0.01%

- Poor long term growth as Operating profit has grown by an annual rate 32.34% of over the last 5 years

- Low ability to service debt as the company has a high Debt to EBITDA ratio of 5.94 times

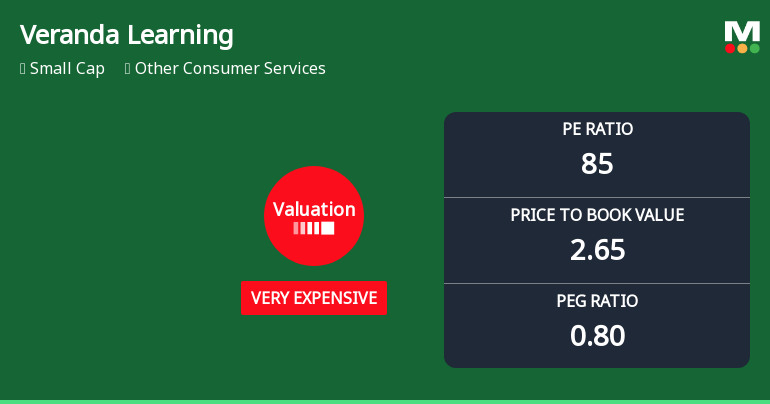

With ROCE of -10.2, it has a Very Expensive valuation with a 2.2 Enterprise value to Capital Employed

30.45% of Promoter Shares are Pledged

Stock DNA

Other Consumer Services

INR 2,442 Cr (Small Cap)

72.00

168

0.00%

0.39

-20.90%

2.59

Total Returns (Price + Dividend)

Veranda Learning for the last several years.

Risk Adjusted Returns v/s

Returns Beta

News

Veranda Learning Solutions Ltd: Valuation Shifts Signal Price Attractiveness Challenges

Veranda Learning Solutions Ltd has experienced a notable shift in its valuation parameters, moving from an already expensive status to very expensive territory. Despite recent strong returns relative to the Sensex, the company’s elevated price-to-earnings (P/E) and price-to-book value (P/BV) ratios, combined with negative profitability metrics, raise concerns about the stock’s price attractiveness and risk profile.

Read More

Veranda Learning Solutions Ltd Surges 7.83% to Day's High of Rs 231.95 — Outperforms Sector by 7.59 Percentage Points

The Sensex eked out a modest gain of 0.17% on 13 May 2026, but Veranda Learning Solutions Ltd surged 7.83%, outperforming its sector by 7.59 percentage points. This sharp single-session advance rewrites the short-term narrative for the small-cap stock, raising the question of whether this is a genuine breakout or a technical bounce within a broader trend.

Read More Announcements

Shareholder Meeting / Postal Ballot-Scrutinizers Report

07-Aug-2026 | Source : BSEPlease find the enclosed Voting Result along with the Scrutinizers Report of the Annual General Meeting of the Company.

Shareholder Meeting / Postal Ballot-Outcome of AGM

06-Aug-2026 | Source : BSEProceedings of 8th Annual General Meeting of the Company.

Board Meeting Intimation for The Un-Audited Financial Results (Standalone And Consolidated) Of The Company For The Quarter Ended June 30 2026

05-Aug-2026 | Source : BSEVeranda Learning Solutions Ltdhas informed BSE that the meeting of the Board of Directors of the Company is scheduled on 13/08/2026 inter alia to consider and approve the Un-audited Financial Results (Standalone and Consolidated) of the Company for the quarter ended June 30 2026

Corporate Actions

13 Aug 2026

No Dividend history available

No Splits history available

No Bonus history available

No Rights history available

Quality key factors

Valuation key factors

Technicals key factors

Technical Indicator Scale: Bearish, Mildly Bearish, Sideways, Mildly Bullish, Bullish Turned

Technical Indicator Scale: Bearish, Mildly Bearish, Sideways, Mildly Bullish, Bullish Turned Shareholding Snapshot : Jun 2026

Shareholding Compare (%holding)

Non Institution

30.4542

Held by 0 Schemes

Held by 22 FIIs (2.83%)

Kalpathi S Aghoram (10.62%)

Authum Investment And Infrastructure Limited (10.81%)

36.78%

Quarterly Results Snapshot (Consolidated) - Mar'26 - QoQ

QoQ Growth in quarter ended Mar 2026 is 13.35% vs -7.84% in Dec 2025

QoQ Growth in quarter ended Mar 2026 is -14.66% vs -89.18% in Dec 2025

Half Yearly Results Snapshot (Consolidated) - Sep'25

Growth in half year ended Sep 2025 is 20.16% vs 15.63% in Sep 2024

Growth in half year ended Sep 2025 is 259.59% vs -178.26% in Sep 2024

Nine Monthly Results Snapshot (Consolidated) - Dec'25

YoY Growth in nine months ended Dec 2025 is 19.36% vs 12.91% in Dec 2024

YoY Growth in nine months ended Dec 2025 is 141.65% vs -555.01% in Dec 2024

Annual Results Snapshot (Consolidated) - Mar'26

YoY Growth in year ended Mar 2026 is 34.60% vs -1.11% in Mar 2025

YoY Growth in year ended Mar 2026 is 142.66% vs -210.32% in Mar 2025

About Veranda Learning Solutions Ltd

Company Coordinates